Australia’s office space seen to be cost-effective

JLL’s Global Premium Office Rent Tracker highlights the affordability of Sydney and Melbourne compared with other global cities

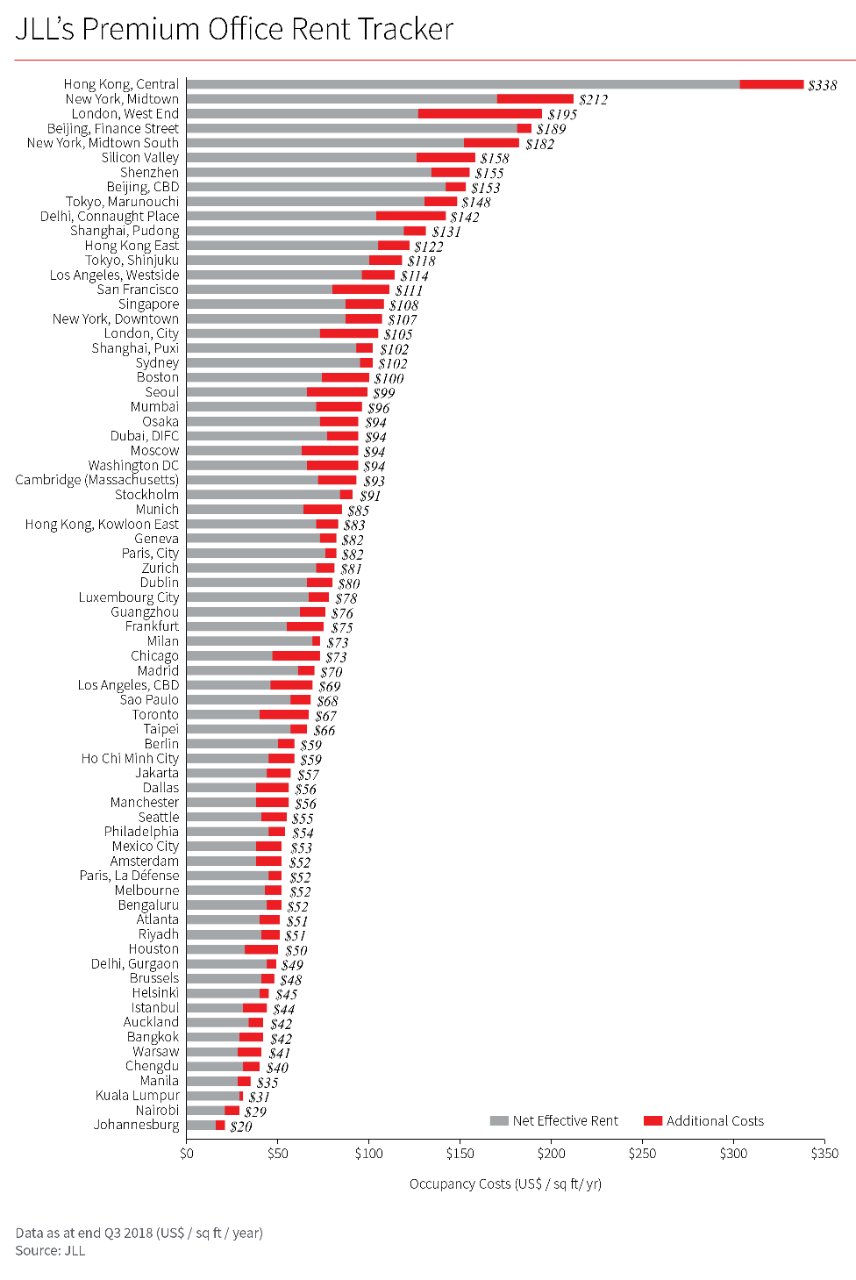

JLL has released its Global Premium Office Rent Tracker covering 72 office submarkets across 61 cities. The Premium Office Rent Tracker is a unique publication which allows occupiers and investors to benchmark rent costs across comparable buildings in global cities.

According to JLL’s Global Premium Office Rent Tracker, the top three most expensive office markets are: Hong Kong’s Central, New York’s Midtown and London’s West End. Sydney is ranked 20th.

Hong Kong’s Central has the world’s most expensive rent for premium offices for the fourth year running. The submarket has occupancy costs – including rent, taxes and service charges – that are 60 per cent more expensive than New York’s Midtown and nearly 75 per cent more expensive than London’s West End.

· Download the Global Premium Office Rent Tracker report here

JLL’s Head of Office Leasing – Australia, Tim O’Connor said, “The key message from the report is the affordability of Sydney and Melbourne compared with other global cities. Sydney is only ranked as the 20th most expensive city, while Melbourne came in at number 56.

“Multi-national organisations are aware that strategic real estate portfolio management can reduce cost and improve the bottom line. While corporate real estate teams ensure that space is used in an efficient manner, more significant cost savings can be made in higher rent markets.

“While we have seen a broadening of the demand base, the finance sector remains important for the Premium Grade office sector. In Sydney, we have seen Asian banks increase their Australian lending activities and become a more relevant part of the Premium Grade occupier market.

“Floorplate efficiency, technical infrastructure, access to a diverse range of F&B options, the provision of third space and high quality end-of-trip facilities make Premium Grade assets attractive to organisations.

“Increasingly, we have seen technology firms attracted to Premium Grade assets, with organisations like Facebook leasing space at Two International Towers Sydney,” Mr O’Connor said.

JLL’s Head of Research – Australia Andrew Ballantyne said: “The increasing diversity of occupiers in Premium Grade office assets is reflective of a desire to attract and retain knowledge workers. The millennial generation is more agnostic to industry sector and attracted to the specific employment opportunity. The location of employer and quality of the physical working environment also forms part of the employment decision making process.”

The strength of Sydney’s Premium Grade sector has resulted in a reduction in vacancy from 14.1% in late 2013 to 4.5% in 3Q18.

The outlook for prime net effective rents in Sydney and Melbourne is positive over 2019. We expect net effective rental growth in both cities of between 5.5% and 6.0%.

Mr O’Connor said, “The underlying demand for Premium Grade space is reflected in the development pipeline. In the Sydney CBD, Wynyard Place, Quay Quarter Tower and Circular Quay Tower will all provide new opportunities for Premium Grade tenants.”

The Melbourne CBD has an under-supply of Premium Grade space with only 8.6% of stock classified as Premium Grade. In comparison the Sydney CBD (20.7%), Perth CBD (19.7%) and Brisbane CBD (11.5%) all have a higher proportion of Premium Grade space than Melbourne.

“The latent demand for Premium Grade assets in Melbourne is reflected in the development pipeline with 477 Collins Street and 80 Collins Street under construction and scheduled to complete in 2019 and 2020,” concluded Mr O’Connor.

Notes

In this fourth edition of JLL’s Premium Office Rent Tracker (PORT), we compare like-for-like occupation costs across 72 major office markets in 61 cities. The 2018 edition includes a further 18 markets from 2017, where we included 54 major markets in 46 cities of differing function and evolution.

Premium office rents refer to the ‘top achievable’ in units over 10,000 square feet (or approximately 1000 square metres) in the premium building in the premier office district of each city. In tall buildings, the middle zone is used as the benchmark. The report excludes rents that represent a premium level paid for a small quantity of space or highly prestigious units where a significant premium applies.

Total occupancy costs are calculated by combining the net effective rent with additional costs (e.g. service charges, taxes).

– ends –

About JLL

JLL (NYSE: JLL) is a leading professional services firm that specializes in real estate and investment management. Our vision is to reimagine the world of real estate, creating rewarding opportunities and amazing spaces where people can achieve their ambitions. In doing so, we will build a better tomorrow for our clients, our people and our communities. JLL is a Fortune 500 company with operations in over 80 countries and a global workforce of 88,000 as of September 30, 2018. JLL is the brand name, and a registered trademark, of Jones Lang LaSalle Incorporated. For further information, visit jll.com