Refurbishment of Australian shopping centres flows on to trading success

Shopping centre managers in JLL survey report refurbishments are the key to retail success in a competitive market

Food and beverage retailing in shopping centres continues to be the stand out performer, while there’s evidence that the impact of refurbishment works is being converted into positive trading results, according to JLL’s latest centre management survey.

JLL’s 19th Retail Centre Managers’ Survey was undertaken in August across 88 JLL-managed retail shopping centres nationally. The majority of centres were neighbourhood and sub-regional centres.[1]

A majority of Centre Managers commented in the survey on the positive impact that store refurbishments by anchor and specialty tenants was having on leasing success, foot traffic and sales performance.

JLL’s Head of Property & Asset Management – Australia, Richard Fennell said, “The Survey showed that 42% of JLL Centre Managers made a positive comment about the recent performance of their centres in relation to an improvement in sales trends, tenant sentiment, foot traffic and/or leasing enquiry.

“We view this as a positive result for the general outlook for the performance of shopping centres.

“Centre Managers were also slightly more optimistic about the outlook for sales, mainly due to factors within their control, such as refurbishments and tenant remix, but had a more negative view on the impact of external factors like ecommerce, the performance of the economy and fuel prices.

“This highlights the importance of active management in the retail sector and is evidence of the value of strategies such as changing the tenancy mix and refurbishment programs to attract foot traffic and customers and improve market share within trade areas.

“The majority of Centre Managers (56%) expected some growth in moving annual turnover (MAT) over the next 12 months.

“JLL Centre Managers continued to view ‘expected changes to tenancy profile’ as having the most positive impact on the MAT outlook or their centres. More than half of survey respondents (61%) stated that it would drive sales growth over the next 12 months, up from 55% in the previous survey in February this year,” said Mr Fennell.

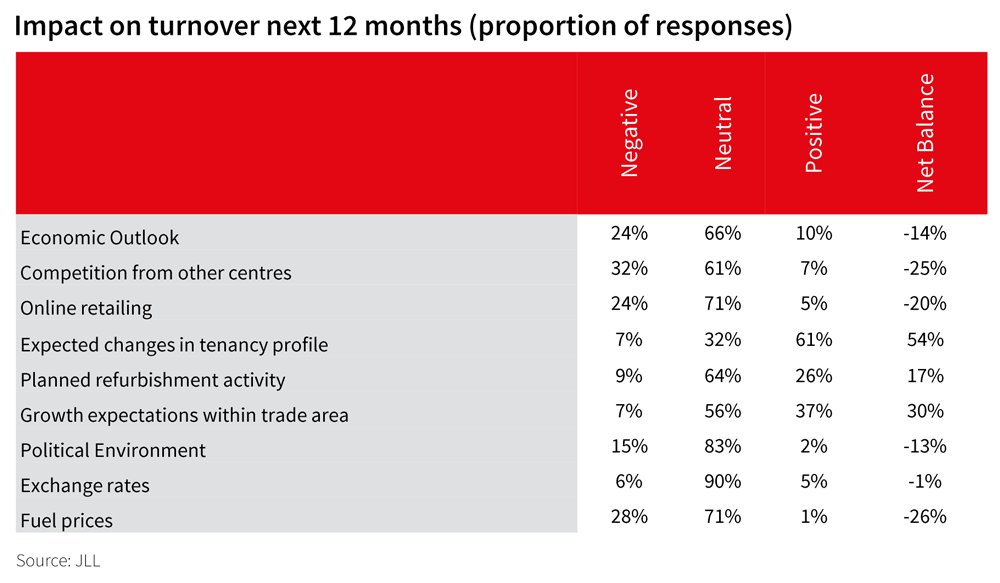

Factors impacting turnover performance – positive and negative

When asked what factors were impacting turnover performance, the strongest positive factors were ‘expected changes in tenancy profile’ (with a net balance of 54%), ‘growth expectations within trade area’ (30%) and ‘planned refurbishment activity’ at 17%

The top three negative factors impacting on turnover have remained consistent with previous surveys. Fuel prices (with a net balance of -26%), competition from other centres (-25%) and online retailing (-20%) remain the top concerns.

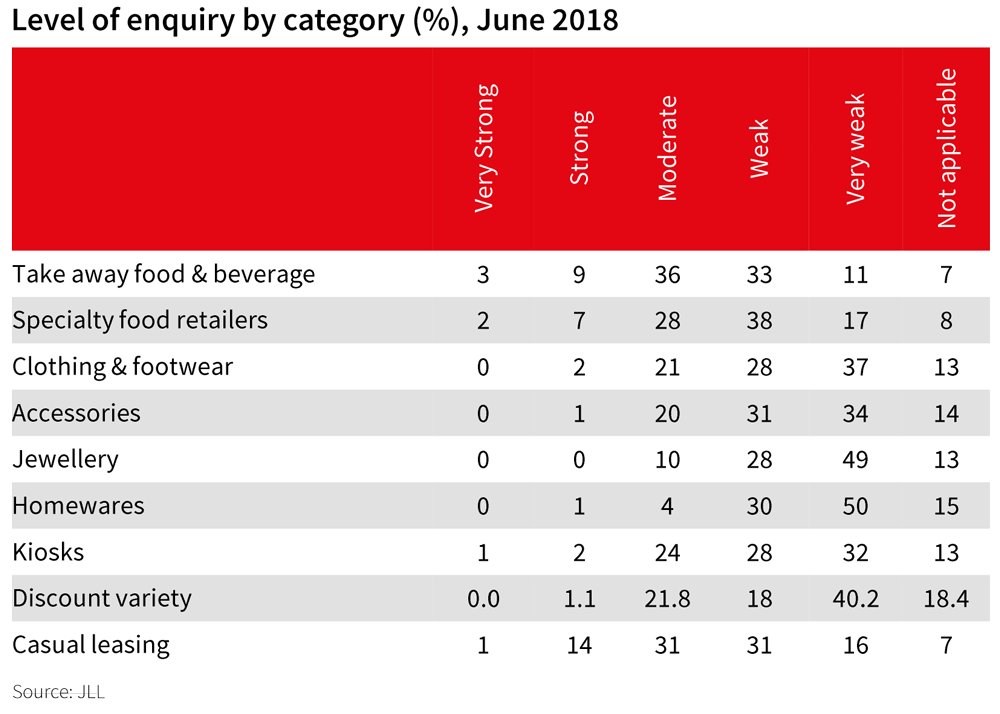

Food operators continue to drive tenant enquiry levels

JLL’s Director of Retail Research, Andrew Quillfeldt said, “Food and Beverage retailers continue to drive leasing enquiry, with 52% of Centre Managers stating that enquiry levels remain the same or stronger than the previous survey.

“It is worth noting that the proportion has softened from previous surveys though, down from 66% in December 2017 and June 2017.

“Enquiry remains subdued in the Jewellery and Homewares categories, with over half of all Centre Managers reporting enquiry as very weak. Clothing and footwear retailer enquiry improved slightly from the previous survey in February, but remains in line with levels reported over the past few years where 74% of respondents reported enquiry was weak or very weak.

“Centre Managers also noted higher incentives were required to secure a new tenant for specialty stores given that tenants are being more selective about where they choose to open new stores.

“Supermarkets are driving total centre MAT growth in neighbourhood and sub-regional centres, with specialty store MAT remaining subdued across the portfolio. The recent improvement in supermarket sales growth was noted by Centre Managers, with 15% commenting on the strong performance of a supermarket within their centre,” said Mr Quillfeldt.

- ends -

1 Classification for shopping centres by sub-sector: Sub-regional centres: Centres that are discount department store based (e.g. Kmart, Target and Big W). Neighbourhood centres: Enclosed centres containing at least one supermarket and specialties.

JLL (NYSE: JLL) is a leading professional services firm that specializes in real estate and investment management. Our vision is to reimagine the world of real estate, creating rewarding opportunities and amazing spaces where people can achieve their ambitions. In doing so, we will build a better tomorrow for our clients, our people and our communities. JLL is a Fortune 500 company with operations in over 80 countries and a global workforce of 88,000 as of September 30, 2018. JLL is the brand name, and a registered trademark, of Jones Lang LaSalle Incorporated. For further information, visit jll.com